Protect Your Savings: Navigating 2026 Inflation & Devaluation Risks

The economic landscape is constantly evolving, and staying ahead of potential shifts is crucial for financial well-being. As we approach 2026, many economists and financial strategists are projecting a significant 2026 inflation outlook, potentially accompanied by a 4% devaluation of currency. This forecast raises critical questions for individuals and businesses alike: How will this impact your savings? What steps can you take to protect your hard-earned money? This comprehensive guide delves into the projected economic challenges and offers actionable strategies to safeguard your financial future.

Understanding the nuances of inflation and currency devaluation is the first step toward effective mitigation. Inflation, at its core, is the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. A 4% devaluation, on the other hand, implies a reduction in the official value of a currency in relation to other currencies or a standard. While these two concepts are distinct, they often move in tandem, creating a formidable challenge for personal and national economies. The 2026 inflation outlook suggests a scenario where both forces could be at play, eroding the value of conventional savings if not properly managed.

Historical data consistently shows that periods of high inflation and currency devaluation can severely diminish wealth. Money held in traditional savings accounts, which typically offer low-interest rates, is particularly vulnerable. For instance, if inflation hits 4% and your savings account yields only 0.5%, you are effectively losing 3.5% of your purchasing power each year. Over time, this can lead to a substantial erosion of wealth. Therefore, a proactive approach is not just advisable; it’s essential.

The Projected 2026 Inflation Outlook: What to Expect

Several factors contribute to the projected 2026 inflation outlook. Global supply chain disruptions, geopolitical tensions, increased government spending, and shifts in consumer demand are all potential drivers. Economic models and expert analyses point towards a continued inflationary pressure, even if at a slower pace than peak periods, making the 4% devaluation forecast a tangible concern. Understanding these underlying causes can help in anticipating market reactions and formulating effective defensive strategies.

One of the primary drivers of inflation is often demand-pull inflation, where aggregate demand in an economy outpaces aggregate supply, leading to higher prices. Another significant factor is cost-push inflation, which occurs when the cost of producing goods and services rises, forcing businesses to increase prices. Both scenarios could contribute to the 2026 inflation outlook. Furthermore, monetary policy decisions by central banks play a pivotal role. If central banks continue to maintain accommodative policies or inject liquidity into the system, it could fuel inflationary pressures.

Currency devaluation can stem from various sources, including large trade deficits, political instability, or a loss of confidence in a country’s economic prospects. A 4% devaluation, while not catastrophic, is significant enough to warrant attention, especially when coupled with inflation. It means that your domestic currency will buy less of foreign goods and services, and imported goods will become more expensive, further feeding into inflationary cycles. This creates a challenging environment where both domestic and international purchasing power are diminished, making the 2026 inflation outlook a dual threat.

For individuals, this means that the cost of living could rise noticeably. Groceries, fuel, housing, and even services could become more expensive. For businesses, this translates to higher input costs, which may or may not be entirely passed on to consumers, impacting profitability. The ripple effect throughout the economy can be profound, affecting everything from investment returns to retirement planning. Therefore, a clear understanding of the 2026 inflation outlook is not just for economists, but for every financially conscious individual.

Strategies to Protect Your Savings from Inflation and Devaluation

Protecting your savings from the anticipated 2026 inflation outlook and devaluation requires a multi-faceted approach. It’s not just about moving money around; it’s about strategic asset allocation, understanding inflation-hedging instruments, and making informed financial decisions. Here are some key strategies:

1. Invest in Inflation-Indexed Securities

One of the most direct ways to combat inflation is to invest in assets specifically designed to protect against it. Treasury Inflation-Protected Securities (TIPS) are a prime example. The principal value of TIPS adjusts with the Consumer Price Index (CPI), ensuring that your investment keeps pace with inflation. When the CPI rises, the principal value of TIPS increases, and vice versa. This adjustment is then used to calculate the interest payments you receive, providing a built-in hedge against rising prices. While their yields might not always be spectacular, their primary purpose is capital preservation in an inflationary environment, making them highly relevant for the 2026 inflation outlook.

Other inflation-indexed securities might include certain types of bonds or funds that track inflation. It’s crucial to research and understand the specific mechanisms by which these securities offer protection, as not all are created equal. Consulting a financial advisor can help in identifying the best options for your specific financial situation and risk tolerance, especially with the looming 2026 inflation outlook.

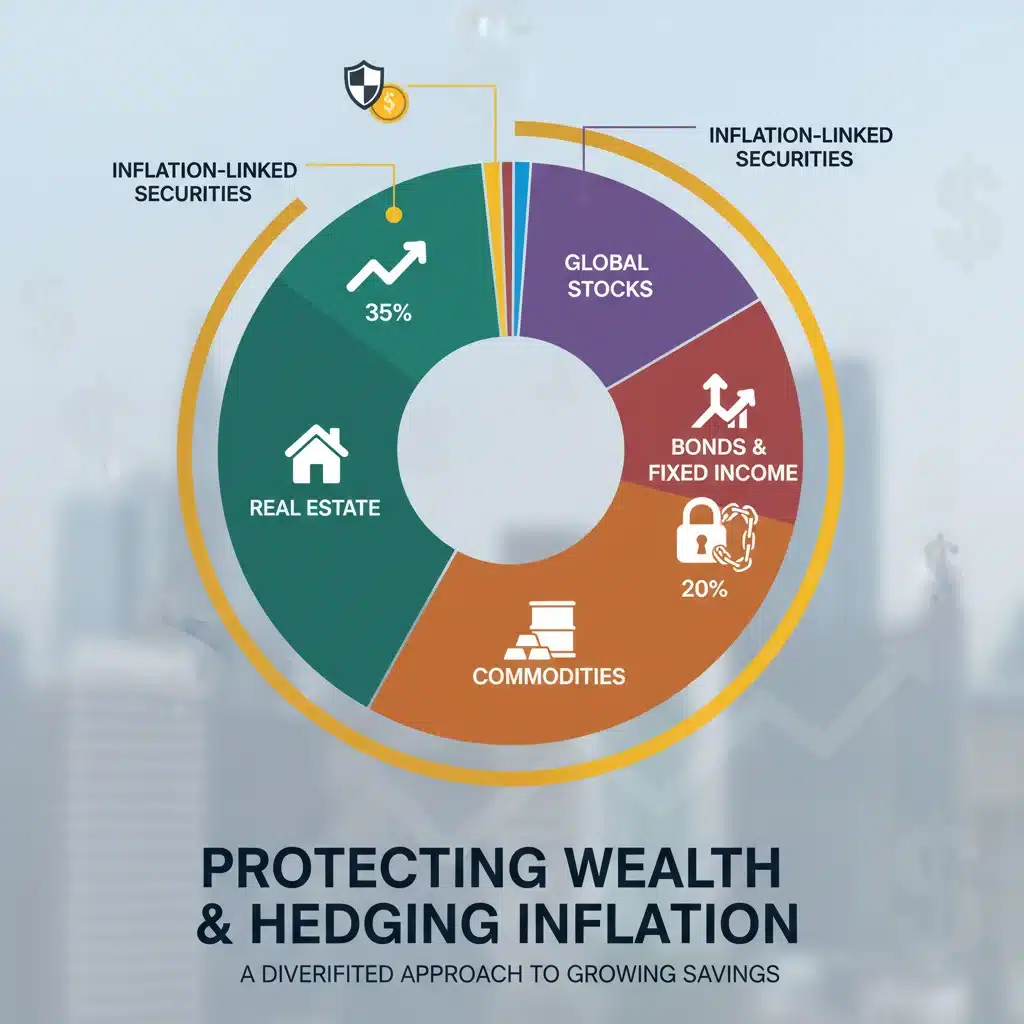

2. Diversify Your Investment Portfolio

Diversification is a cornerstone of sound investment strategy, and it becomes even more critical during periods of economic uncertainty. A well-diversified portfolio spreads risk across various asset classes, reducing the impact of poor performance in any single asset. When facing the 2026 inflation outlook, this means considering assets that historically perform well during inflationary periods.

Consider including real assets such as real estate, commodities (like gold, silver, oil), and infrastructure. Real estate, for instance, often appreciates in value with inflation, and rental income can also increase, providing a dual benefit. Commodities tend to be direct beneficiaries of rising prices, as they are the raw materials for many goods. Gold, in particular, has long been considered a safe-haven asset during times of economic instability and inflation. While not guaranteed, its historical performance suggests it can be a valuable component in mitigating the effects of the 2026 inflation outlook.

3. Consider Real Estate Investments

Real estate has a strong track record as an inflation hedge. As the cost of living increases, so too do property values and rental rates. Investing in income-generating properties can provide a steady stream of revenue that adjusts with inflation, while the underlying asset appreciates. This can include residential properties, commercial real estate, or even Real Estate Investment Trusts (REITs), which allow you to invest in real estate without directly owning physical property. REITs can offer liquidity and diversification that direct property ownership might not, making them an attractive option for many investors concerned about the 2026 inflation outlook.

However, real estate investments are not without risk. Factors such as interest rate hikes, local market conditions, and property management challenges can impact returns. Thorough due diligence and a long-term perspective are essential when incorporating real estate into your inflation-fighting strategy.

4. Invest in Stocks of Companies with Pricing Power

Not all stocks are created equal when it comes to inflation. Companies that possess strong ‘pricing power’ – meaning they can raise their prices without significant loss of sales volume – tend to perform better during inflationary periods. These are often companies with strong brands, essential products or services, or those operating in industries with high barriers to entry. Examples might include certain consumer staples, technology giants, or healthcare companies. Their ability to pass on increased costs to consumers helps maintain profit margins, offering a degree of protection against the 2026 inflation outlook.

Conversely, companies with thin margins, high debt, or those operating in highly competitive industries may struggle as their input costs rise and they are unable to fully pass those costs on. Careful stock selection and fundamental analysis are key to identifying resilient businesses in an inflationary environment.

5. Evaluate Your Debt

In an inflationary environment, the value of money decreases over time, which can actually be beneficial for borrowers with fixed-rate debt. The real value of your debt diminishes as inflation erodes the purchasing power of the money you owe. This is why some financial advisors suggest that holding fixed-rate mortgages or other fixed-rate loans can be a strategic move during periods of high inflation. However, it’s a double-edged sword: if you have variable-rate debt, rising interest rates (often a central bank’s response to inflation) could significantly increase your monthly payments.

Therefore, it’s prudent to evaluate your current debt structure. If you have significant variable-rate debt, consider refinancing to a fixed rate if market conditions are favorable. Reducing high-interest consumer debt, regardless of inflation, is always a wise financial move. This proactive step can free up capital that can then be deployed into inflation-hedging assets, strengthening your position against the 2026 inflation outlook.

6. Consider Foreign Currencies and International Investments

Given the projection of a 4% devaluation, investing in strong foreign currencies or international assets can be a way to hedge against domestic currency weakness. Currencies of countries with strong economic fundamentals, low inflation, or attractive interest rates might offer better stability. This can be done through foreign currency exchange-traded funds (ETFs), international bond funds, or direct investments in foreign stocks. However, this strategy comes with its own set of risks, including currency exchange rate fluctuations, geopolitical risks, and different regulatory environments.

It’s vital to conduct thorough research and understand the economic conditions of the countries whose currencies or assets you are considering. Diversifying internationally can provide a layer of protection against localized economic downturns and currency devaluation, making it a viable option to consider in light of the 2026 inflation outlook.

7. Review Your Emergency Fund

An emergency fund is critical for financial security, but its effectiveness can be eroded by inflation. If your emergency fund is held in a low-yield savings account, its purchasing power will diminish. While you shouldn’t put your emergency fund at significant risk, consider options that offer slightly better returns while maintaining liquidity. High-yield savings accounts, money market accounts, or short-term certificates of deposit (CDs) that are inflation-indexed could be suitable alternatives. The goal is to ensure that your emergency fund retains its real value, or at least loses less value, so it can still cover several months of living expenses when needed, especially with the 2026 inflation outlook in mind.

Regularly review the size of your emergency fund. As the cost of living increases due to inflation, the amount needed to cover three to six months of expenses will also rise. Adjust your fund accordingly to maintain its efficacy.

8. Invest in Yourself: Skills and Education

While often overlooked in financial discussions, investing in your human capital is one of the most powerful inflation hedges. Acquiring new skills, pursuing further education, or gaining certifications can increase your earning potential. Higher income means greater capacity to absorb rising costs and allocate more funds towards inflation-protected investments. In an economy where the value of money is fluctuating, your ability to generate income becomes an invaluable asset. This strategy offers long-term benefits that extend beyond just mitigating the 2026 inflation outlook.

Consider what skills are in demand and how you can enhance your professional value. This could involve online courses, vocational training, or even pursuing a higher degree. The return on investment in education and skills can often outpace traditional financial investments, especially in uncertain economic times.

9. Seek Professional Financial Advice

Navigating the complexities of inflation and currency devaluation can be challenging, even for seasoned investors. A qualified financial advisor can provide personalized guidance based on your specific financial situation, risk tolerance, and goals. They can help you assess the potential impact of the 2026 inflation outlook on your portfolio, recommend appropriate investment strategies, and assist in creating a comprehensive financial plan designed to protect and grow your wealth.

When choosing a financial advisor, look for someone who is a fiduciary, meaning they are legally obligated to act in your best interest. Discuss their experience with inflation hedging strategies and their understanding of current economic forecasts. A good advisor will help you make informed decisions and adjust your strategy as economic conditions evolve.

Understanding the Long-Term Implications of Inflation

The 2026 inflation outlook is not just a short-term blip; it could have long-term implications for retirement planning, wealth transfer, and overall financial stability. Sustained inflation erodes the purchasing power of pensions, fixed income streams, and traditional savings. This means that the amount of money you thought would be sufficient for retirement might fall short, requiring adjustments to your spending habits or a need to generate more income.

For those nearing retirement, the focus shifts even more towards capital preservation and generating inflation-adjusted income. Strategies might include annuities that offer inflation protection, or a higher allocation to dividend-paying stocks from companies with strong pricing power. For younger individuals, the emphasis should be on maximizing earning potential and aggressively investing in growth assets that have historically outpaced inflation over the long term.

Moreover, the psychological impact of inflation cannot be underestimated. A constant rise in prices can lead to anxiety and uncertainty about the future. By proactively addressing the 2026 inflation outlook and implementing robust financial strategies, you can gain peace of mind and maintain confidence in your financial future.

Conclusion: Proactive Steps for a Secure Financial Future

The projected 2026 inflation outlook and a potential 4% devaluation present a clear call to action for individuals and businesses to reassess their financial strategies. While economic forecasts are never certain, being prepared for potential challenges is always prudent. By understanding the mechanisms of inflation and devaluation, and by implementing a combination of strategic investments and sound financial planning, you can significantly mitigate the risks to your savings.

From investing in inflation-indexed securities and diversifying across real assets and stocks with pricing power, to optimizing your debt and seeking expert advice, there are numerous avenues to explore. The key is to be proactive, informed, and adaptable. Don’t let your savings erode passively; take control of your financial destiny and ensure your wealth is protected against the anticipated economic shifts. The time to prepare for the 2026 inflation outlook is now, ensuring a more secure and prosperous financial future for yourself and your loved ones.

Remember that financial planning is an ongoing process. Regularly review your portfolio, stay informed about economic trends, and be prepared to adjust your strategies as circumstances change. With careful planning and disciplined execution, you can navigate the challenges of inflation and devaluation and emerge stronger.

Contributions 2026: Maximize Retirement Savings")