2026 Social Security COLA: What a 3.2% Increase Means for You

In the world of retirement planning, few announcements carry as much weight and generate as much discussion as the annual Social Security Cost-of-Living Adjustment, or COLA. For millions of retirees, disabled individuals, and survivors, this adjustment is a critical component of their financial well-being, directly impacting the purchasing power of their monthly benefits. As we look ahead, projections for the 2026 Social Security COLA are beginning to emerge, with a significant 3.2% increase currently anticipated. This figure, while still a projection and subject to change, offers a vital glimpse into the financial landscape that Social Security beneficiaries can expect in the coming years. Understanding what a 3.2% COLA means for your monthly payments, and the broader implications for your financial planning, is essential for navigating the complexities of retirement in an ever-evolving economic environment.

The Social Security Administration (SSA) implements COLA to ensure that the purchasing power of Social Security benefits is not eroded by inflation. Without these annual adjustments, the fixed income of beneficiaries would steadily decline in real terms, making it increasingly difficult to cover essential living expenses. The calculation of COLA is tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a measure of inflation that tracks changes in the prices of goods and services. While the final COLA figure is typically announced in October of the preceding year, early projections, such as the anticipated 3.2% for 2026, provide valuable insights for individuals and families to begin their financial preparations. This article will delve into the mechanics of COLA, explore the potential impact of a 3.2% increase on various income levels, and offer actionable strategies for beneficiaries to optimize their financial outlook in light of these adjustments.

The significance of the 2026 Social Security COLA cannot be overstated. A 3.2% increase, if realized, would represent a substantial boost for many, helping to offset the rising costs of housing, food, healthcare, and other necessities. However, it’s also crucial to consider the nuances of this adjustment. While a higher COLA can bring welcome relief, it can also have ripple effects on other aspects of a beneficiary’s financial life, including potential impacts on Medicare premiums, income tax liabilities, and eligibility for certain low-income assistance programs. Therefore, a comprehensive understanding of the 2026 Social Security COLA is not just about knowing the percentage; it’s about grasping its multifaceted influence on your overall financial picture. Join us as we unpack these details, offering clarity and guidance for all those who rely on Social Security benefits.

Understanding the Social Security COLA: The Basics

Before we dive into the specifics of the projected 3.2% 2026 Social Security COLA, it’s essential to grasp the fundamental principles behind the Cost-of-Living Adjustment. What exactly is COLA, why is it necessary, and how is it determined? These are crucial questions for anyone receiving or anticipating Social Security benefits.

What is COLA?

COLA stands for Cost-of-Living Adjustment. It is an annual increase in Social Security and Supplemental Security Income (SSI) benefits to counteract the effects of inflation. The primary goal of COLA is to maintain the purchasing power of these benefits over time. Without COLA, the fixed dollar amount of benefits would gradually buy less as the cost of goods and services rises, effectively eroding the financial security of beneficiaries.

Why is COLA Necessary?

Inflation is a persistent economic phenomenon where the general price level of goods and services in an economy increases over a period. This means that a dollar today buys less than it did yesterday. For individuals living on fixed incomes, such as Social Security beneficiaries, inflation can be particularly challenging. Their income doesn’t automatically adjust to the rising costs of living, leading to a decline in their real income. COLA serves as a vital safeguard, ensuring that retirees, survivors, and individuals with disabilities can continue to afford essential items like food, housing, healthcare, and transportation.

How is COLA Calculated?

The Social Security Act mandates that COLA be calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This specific index measures the average change over time in the prices paid by urban wage earners and clerical workers for a market basket of consumer goods and services. The calculation process involves several steps:

- Reference Period: The SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the last year in which a COLA was payable.

- Percentage Increase: The percentage increase in the CPI-W from the base quarter to the current year’s third quarter average determines the COLA.

- Rounding: If the calculated percentage increase is not a multiple of one-tenth of one percent, it is rounded to the nearest one-tenth of one percent.

- No Decrease: Importantly, Social Security benefits cannot decrease due to COLA. If there is no increase in the CPI-W or a decrease, there will be no COLA for that year, and benefits remain unchanged.

For example, to determine the 2026 Social Security COLA, the SSA will compare the average CPI-W for the third quarter of 2025 with the average CPI-W for the third quarter of 2024 (assuming a COLA was payable in 2025). The resulting percentage increase will be the COLA applied to benefits starting in January 2026.

The Role of CPI-W vs. CPI-U

It’s worth noting that the CPI-W differs from the more commonly cited Consumer Price Index for All Urban Consumers (CPI-U). While both measure inflation, the CPI-W focuses on the spending patterns of urban wage earners and clerical workers, which tend to have a higher proportion of transportation and food costs compared to the CPI-U, which covers a broader segment of the population. Critics often argue that the CPI-W may not fully reflect the expenditure patterns of seniors, particularly their higher healthcare costs. However, current law specifies the use of CPI-W for COLA calculations.

Understanding these foundational aspects of COLA provides the necessary context to appreciate the potential impact of the projected 3.2% increase for 2026. This adjustment is not a discretionary bonus but a critical mechanism designed to preserve the purchasing power of millions of Americans.

Projected 3.2% COLA for 2026: What It Means for Your Payments

The anticipation of a 3.2% 2026 Social Security COLA is a significant development for current and future beneficiaries. While this figure is still a projection and subject to change based on economic data throughout 2025, it offers a valuable estimate of the potential increase in monthly Social Security payments. Let’s break down what a 3.2% adjustment could mean for your benefits.

Calculating Your Potential Increase

The calculation is straightforward: your current monthly Social Security benefit would be multiplied by 3.2%. For instance:

- If your current monthly benefit is $1,000, a 3.2% COLA would add $32 to your payment, bringing it to $1,032.

- For a benefit of $1,500, the increase would be $48, resulting in a new payment of $1,548.

- If you receive $2,000 per month, your benefit would increase by $64, totaling $2,064.

- For those with higher benefits, say $3,000, the increase would be $96, making the new payment $3,096.

These examples illustrate that even what might seem like a modest percentage increase can translate into a meaningful boost in monthly income, especially for those who rely heavily on Social Security for their living expenses.

Impact on Average Benefits

To provide a broader perspective, let’s consider the average Social Security benefits. While the exact average for 2025 is not yet finalized, we can use current averages as a baseline. For example, if the average retired worker’s benefit is around $1,900 per month, a 3.2% COLA would add approximately $60.80 to their monthly check. For an average couple receiving benefits, the increase would be even more substantial.

This increase helps to bridge the gap between fixed incomes and rising costs. However, it’s important to remember that averages can be misleading. Individual circumstances, such as your work history, earnings record, and age at which you claimed benefits, will determine your specific monthly payment and thus the exact dollar amount of your COLA increase.

When Will This Increase Take Effect?

The 2026 Social Security COLA, once officially announced in October 2025, will apply to benefits paid starting in January 2026. This means that beneficiaries will see the increased amount in their Social Security checks or direct deposits beginning in the first month of the new year.

Beyond the Dollar Amount: Real Purchasing Power

While the dollar amount of the increase is important, the true significance of COLA lies in its ability to preserve purchasing power. If inflation continues at a rate similar to the 3.2% COLA, then your increased benefits should theoretically allow you to buy the same amount of goods and services as you could before the price increases. However, if inflation outpaces the COLA, or if your personal inflation rate (due to specific spending habits, especially on healthcare) is higher than the CPI-W, then even with a COLA, your real purchasing power might still experience some erosion.

Therefore, while a 3.2% COLA is a positive sign, it’s crucial for beneficiaries to monitor their personal expenses and overall economic conditions to fully understand the real-world impact on their financial security. This projected increase serves as a strong reminder to regularly review your budget and financial plan.

Factors Influencing the 2026 COLA Projection and Future Outlook

The projected 3.2% for the 2026 Social Security COLA is not a random number; it’s the result of complex economic forecasts and the underlying factors that drive inflation. Understanding these influences is key to appreciating why the COLA is what it is, and what might cause it to shift before the final announcement.

Key Economic Indicators Driving COLA

As established, the CPI-W is the primary determinant of COLA. Therefore, any factors that affect the CPI-W will directly influence the COLA projection. These include:

- Energy Prices: Fluctuations in the cost of oil, natural gas, and electricity have a significant impact on the CPI-W. Higher energy prices translate into higher transportation costs for goods and services, and increased utility bills for consumers, pushing inflation upwards.

- Food Prices: The cost of groceries is another major component of the CPI-W. Factors like weather patterns, supply chain disruptions, global commodity prices, and agricultural policies can all affect food inflation.

- Housing Costs: Rent and owners’ equivalent rent (OER) are substantial components of the CPI-W. Rising housing costs in urban areas can contribute significantly to inflationary pressures.

- Supply Chain Dynamics: Global and domestic supply chain issues, as witnessed in recent years, can lead to shortages and increased costs for various goods, contributing to overall inflation.

- Labor Market Conditions: Strong wage growth can lead to businesses passing on higher labor costs to consumers through increased prices, feeding into inflation.

- Monetary Policy: Actions by the Federal Reserve, such as interest rate adjustments, aim to control inflation. High interest rates can cool down the economy and reduce inflationary pressures, while lower rates can stimulate demand and potentially lead to higher inflation.

The 3.2% projection for the 2026 Social Security COLA is based on current expectations for these economic indicators throughout 2025. If inflation decelerates more rapidly than anticipated, the final COLA could be lower. Conversely, if inflationary pressures persist or intensify, the final COLA could be higher.

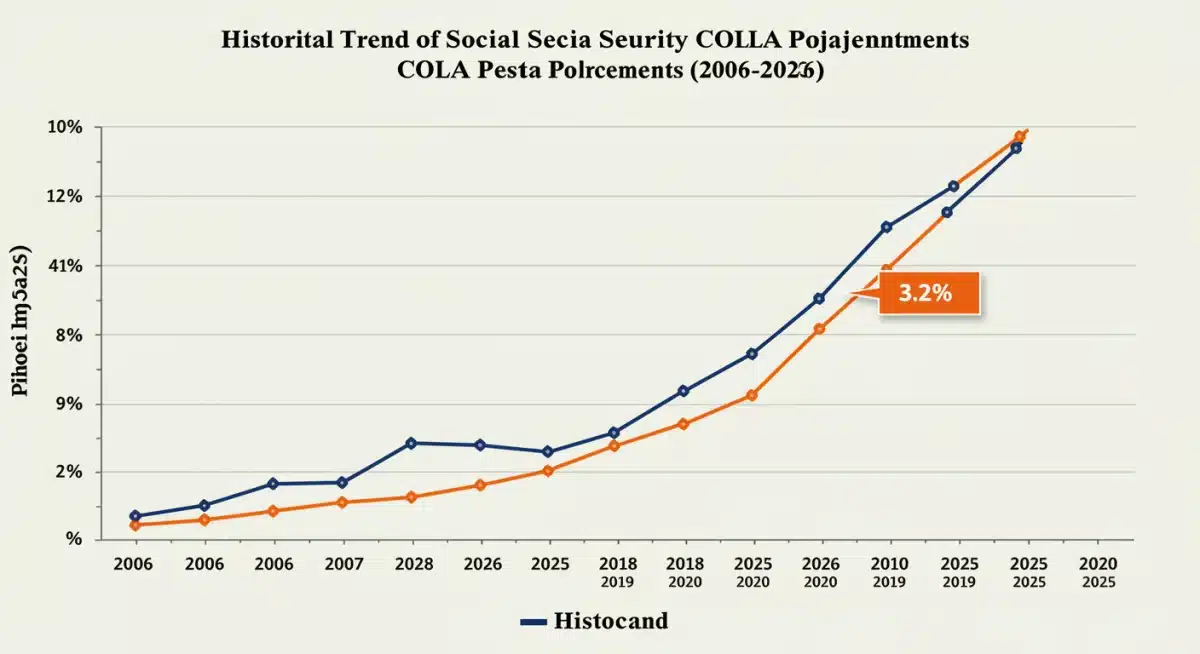

Historical COLA Trends

Looking at historical COLA figures provides valuable context. Over the past few decades, COLA has varied significantly, reflecting different economic periods:

- Periods of High Inflation: In the late 1970s and early 1980s, COLA figures were in the double digits, reflecting periods of rampant inflation.

- Periods of Low Inflation: More recently, there have been years with very low or even zero COLA, particularly after economic downturns when inflation was subdued.

- Recent Volatility: The last few years have seen higher COLA figures due to elevated inflation, demonstrating the responsiveness of the adjustment mechanism to economic shifts.

A 3.2% COLA would be considered a moderate to strong adjustment compared to the average over the last two decades, reflecting ongoing inflationary pressures while potentially indicating a moderation from the higher COLA figures seen in the immediate post-pandemic period.

Future Economic Outlook and Potential Shifts

Several factors could influence the final 2026 Social Security COLA between now and October 2025:

- Geopolitical Events: Conflicts, trade disputes, or other international events can disrupt supply chains and commodity markets, leading to unexpected inflationary spikes or drops.

- Energy Market Volatility: Oil prices are notoriously volatile. A sudden surge or collapse in global oil prices could significantly alter inflation forecasts.

- Economic Growth: Strong economic growth generally correlates with higher demand and potentially higher inflation. A slowdown or recession could suppress inflation.

- Federal Reserve Actions: Future interest rate decisions by the Federal Reserve will play a crucial role in shaping the inflationary environment.

Beneficiaries should remain aware that the 3.2% projection is an estimate. It’s a useful tool for preliminary financial planning, but the final figure will depend on actual economic data observed in the third quarter of 2025. Staying informed about economic news and official announcements from the Social Security Administration will be crucial as we approach the final determination.

Beyond the COLA: Other Financial Considerations for Beneficiaries

While the 3.2% 2026 Social Security COLA is a central piece of your financial puzzle, it’s crucial to understand that it doesn’t operate in a vacuum. Other financial factors can significantly impact the net benefit you receive and your overall financial health. A holistic view is essential for effective retirement planning.

Medicare Part B Premiums

One of the most significant considerations for many Social Security beneficiaries is Medicare Part B premiums. These premiums are often deducted directly from Social Security checks. By law, the “hold harmless” provision generally prevents an individual’s net Social Security benefit from decreasing year-to-year due to an increase in Medicare Part B premiums. However, this provision doesn’t apply to everyone, especially those new to Medicare or those whose Part B premiums are already covered by state programs.

More importantly, an increase in COLA can sometimes be fully or partially offset by a rise in Medicare Part B premiums. For instance, if your Social Security benefit increases by $50 due to COLA, but your Medicare Part B premium also increases by $30, your net increase in spendable income is only $20. It’s vital to factor in anticipated changes to Medicare costs when evaluating the real impact of the 2026 Social Security COLA.

Income Taxation of Social Security Benefits

Another crucial, often overlooked, aspect is the potential for Social Security benefits to become taxable. Depending on your “combined income” (which includes your adjusted gross income, tax-exempt interest, and half of your Social Security benefits), a portion of your Social Security benefits may be subject to federal income tax. The thresholds for taxation have not been adjusted for inflation since they were introduced, meaning that over time, more beneficiaries find their benefits subject to taxation.

- Up to 50% of benefits taxed: If your combined income is between $25,000 and $34,000 for an individual, or between $32,000 and $44,000 for a married couple filing jointly.

- Up to 85% of benefits taxed: If your combined income is above $34,000 for an individual or above $44,000 for a married couple filing jointly.

A 3.2% increase in your Social Security benefit could potentially push your combined income over one of these thresholds, or further into a taxable bracket, leading to a higher tax liability. This effectively reduces the net gain from the COLA. It’s advisable to consult with a tax professional to understand how the 2026 Social Security COLA might affect your personal tax situation.

Impact on Other Government Benefits

For individuals who receive other needs-based government benefits, such as Supplemental Security Income (SSI), Medicaid, or housing assistance, an increase in Social Security benefits due to COLA could potentially affect their eligibility or the amount of those other benefits. While Social Security COLA is designed to protect purchasing power, some programs have strict income limits. An increase, even a modest one, could inadvertently push an individual over these limits, leading to a reduction or loss of other crucial assistance. It’s important to review the income thresholds for any other benefits you receive.

Personal Inflation Rate vs. CPI-W

As mentioned earlier, the COLA is based on the CPI-W. However, your personal inflation rate may differ significantly from this general index. For example, if a large portion of your budget is dedicated to healthcare costs, which often rise faster than general inflation, then a 3.2% COLA might not fully cover your increased expenses. Similarly, if you have specific dietary needs or live in an area with particularly high housing cost increases, your personal experience of inflation could be higher than the national average reflected in the CPI-W.

Therefore, while the 2026 Social Security COLA provides a general adjustment, it’s critical to maintain a detailed personal budget and regularly review your spending to ensure your income keeps pace with your actual cost of living.

By considering these additional financial factors alongside the COLA, beneficiaries can develop a more realistic and comprehensive financial plan for their retirement years.

Strategies for Financial Planning with the 2026 Social Security COLA

The projected 3.2% 2026 Social Security COLA offers an opportunity for beneficiaries to reassess and refine their financial strategies. While it provides a welcome boost, proactive planning is essential to maximize its benefits and mitigate any potential downsides. Here are several strategies to consider:

1. Re-evaluate Your Budget

With an anticipated increase in your monthly Social Security income, now is an excellent time to revisit your household budget. Consider where the extra funds can be most effectively allocated:

- Covering Rising Costs: Prioritize using the COLA increase to offset increases in essential expenses like groceries, utilities, and transportation that may have occurred due to inflation.

- Healthcare Costs: Factor in potential increases in Medicare premiums, deductibles, and out-of-pocket medical expenses. The COLA might help absorb some of these rising healthcare burdens.

- Debt Reduction: If you have high-interest debt (e.g., credit card balances), channeling the COLA increase towards paying it down can significantly improve your financial health in the long run.

- Savings and Emergency Fund: Even in retirement, maintaining an adequate emergency fund is crucial. Consider directing a portion of the COLA increase to bolster your savings for unexpected expenses.

2. Assess Your Tax Situation

As discussed, an increase in Social Security benefits can impact the taxation of your benefits. Proactively assess your tax liability:

- Consult a Tax Professional: Before the end of 2025, speak with a tax advisor to understand how the 2026 Social Security COLA might affect your combined income and potential tax obligations for the 2026 tax year.

- Adjust Withholding: If necessary, you might need to adjust your income tax withholding or make estimated tax payments to avoid a surprise tax bill.

- Review Other Income Sources: Consider how the COLA interacts with withdrawals from IRAs, 401(k)s, or other taxable income sources. Strategic planning here can help manage your overall tax burden.

3. Review Investment and Savings Plans

For those with additional savings or investments, the COLA adjustment can be a trigger to review your broader financial portfolio:

- Inflation Protection: Ensure your investment strategy adequately accounts for inflation. While COLA helps with Social Security, your other assets also need to maintain their purchasing power.

- Withdrawal Rates: If you’re following a specific retirement withdrawal strategy, recalibrate it to reflect the updated Social Security income and current economic forecasts.

- Long-Term Care Planning: Rising healthcare costs are a major concern. Use the opportunity to review your long-term care insurance or savings dedicated to future medical needs.

4. Stay Informed and Adapt

Economic conditions are dynamic, and the final 2026 Social Security COLA will be confirmed in October 2025. It’s crucial to stay informed:

- Monitor Official Announcements: Keep an eye on announcements from the Social Security Administration regarding the final COLA figure and any accompanying information regarding Medicare premiums.

- Economic News: Follow reputable economic news sources to understand broader inflation trends and their potential impact on your finances.

- Flexibility: Be prepared to adapt your financial plan if the economic landscape or the final COLA figure differs significantly from current projections.

5. Maximize Other Benefits (If Applicable)

If you are eligible for, or are considering applying for, other government assistance programs, understand how the COLA might affect your eligibility. Some programs have income limits that are not indexed to inflation in the same way Social Security benefits are. Research these program rules carefully.

By taking a proactive and comprehensive approach to financial planning in light of the projected 3.2% 2026 Social Security COLA, beneficiaries can better secure their financial future and ensure their benefits continue to support their desired quality of life.

The Broader Implications of COLA for Retirement Security

The annual Social Security Cost-of-Living Adjustment, including the projected 3.2% 2026 Social Security COLA, extends its influence far beyond individual monthly checks. It plays a critical role in the broader landscape of retirement security, impacting economic stability for seniors, the solvency of the Social Security system, and the overall national economy.

Maintaining Senior Living Standards

For millions of Americans, Social Security is the primary, or even sole, source of retirement income. COLA directly contributes to maintaining the living standards of these individuals. Without these adjustments, the fixed income of retirees would steadily lose value due to inflation, forcing many into difficult choices between necessities like food, housing, and healthcare. A robust COLA helps prevent a significant decline in the quality of life for seniors, allowing them to better manage increasing costs without having to dip deeper into limited savings or, worse, fall into poverty.

The 2026 Social Security COLA, if it materializes at 3.2%, would represent a meaningful effort to keep pace with the ongoing cost of living, providing a necessary buffer against economic erosion for a vulnerable population segment.

Impact on Social Security Solvency

While beneficial for recipients, COLA also has implications for the long-term solvency of the Social Security trust funds. Each COLA increase means a higher payout from the system. In years with high inflation, and consequently high COLA, the payouts increase substantially, putting additional strain on the system’s finances. The Social Security Trustees regularly issue reports on the financial health of the system, projecting when the trust funds might be depleted if no legislative changes are made.

The balance between providing adequate benefits to current retirees and ensuring the long-term viability of the system for future generations is a constant challenge. A 3.2% COLA, while moderate, must be viewed within the context of the system’s overall financial health and demographic trends. Debates around how COLA is calculated (e.g., using a different inflation index like the Chained CPI) often arise in discussions about Social Security reform, aiming to potentially reduce the rate of benefit growth to improve solvency, albeit at the cost of lower real benefits for retirees.

Economic Stimulus and Consumer Spending

The aggregate increase in Social Security benefits due to COLA represents a significant injection of funds into the economy. Seniors, especially those on fixed incomes, tend to have a high propensity to consume, meaning they spend a larger portion of any additional income rather than saving it. This increased consumer spending can provide a modest stimulus to local and national economies, supporting businesses and jobs.

The projected 3.2% 2026 Social Security COLA will translate into billions of dollars of additional spending power for millions of Americans, which can help support economic activity, particularly in sectors heavily reliant on senior consumers such as healthcare, retail, and services.

Influence on Retirement Planning and Personal Finance

For individuals still in their working years, the consistency and predictability of COLA are important factors in retirement planning. Knowing that their future Social Security benefits will be adjusted for inflation provides a level of certainty and reduces the risk of outliving their savings due to rising costs. Financial advisors often incorporate projected COLA rates into their models when helping clients plan for retirement income streams.

However, it also highlights the importance of diversified retirement savings. While COLA helps preserve the value of Social Security, relying solely on these benefits can be risky. Personal savings, investments, and pensions (if applicable) remain crucial components of a robust retirement plan, offering additional layers of inflation protection and financial flexibility.

In conclusion, the 2026 Social Security COLA is more than just a percentage; it’s a vital economic mechanism with far-reaching implications for individual welfare, systemic sustainability, and the broader economy. Understanding its role is fundamental to comprehending the dynamics of retirement in America.

Conclusion: Preparing for the 2026 Social Security COLA

The projected 3.2% 2026 Social Security COLA stands as a significant marker for millions of Americans who rely on these crucial benefits. While it remains a projection until the official announcement in October 2025, this anticipated increase offers a valuable opportunity for proactive financial planning. Understanding the mechanics of COLA, its potential impact on your monthly payments, and its broader implications for your financial landscape is not merely an academic exercise; it’s an essential step toward securing your retirement future.

We’ve explored how the COLA is calculated, primarily driven by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), and how factors like energy prices, food costs, and housing influence these projections. A 3.2% increase, if realized, would mean a tangible boost in monthly income, helping beneficiaries to better keep pace with the rising cost of living that is an inevitable part of our economic environment. For an average beneficiary, this could translate into dozens of additional dollars each month, providing welcome relief and increased purchasing power.

However, the impact of the 2026 Social Security COLA extends beyond the simple percentage increase. We’ve highlighted the critical need to consider how this adjustment might interact with other financial elements of your life. Potential increases in Medicare Part B premiums, the income taxation of Social Security benefits, and the eligibility for other needs-based government programs are all factors that can significantly influence the net benefit you ultimately receive. Therefore, a holistic approach to financial planning is paramount.

To effectively navigate these changes, we’ve outlined several actionable strategies. Re-evaluating your budget to allocate the increased funds wisely, assessing your tax situation with the help of a professional, reviewing your broader investment and savings plans, and staying informed about official announcements are all crucial steps. By taking proactive measures, you can ensure that the COLA works in your favor, helping to maintain your financial stability and quality of life in retirement.

Ultimately, the 2026 Social Security COLA underscores the importance of Social Security as a foundational pillar of retirement security in the United States. While the system faces its own long-term challenges, the annual COLA mechanism remains a vital tool for protecting the purchasing power of current beneficiaries. By understanding its intricacies and planning accordingly, you can empower yourself to make informed decisions and adapt to the evolving economic landscape, ensuring a more secure and comfortable retirement.

Stay tuned for the official COLA announcement in October 2025, and continue to prioritize your financial planning to make the most of your Social Security benefits.