Cut Student Loan Interest: Strategies for 2026 Federal Policies

For millions of Americans, student loan debt is a significant financial burden, often stretching for decades and impacting major life decisions. The interest accrued on these loans can add tens of thousands of dollars to the principal amount, making repayment an uphill battle. However, with the right strategies and a keen understanding of evolving federal policies, it’s possible to significantly reduce your student loan interest, potentially by up to 1.5% or more, especially as we look towards 2026. This comprehensive guide will equip you with the knowledge and actionable steps to navigate the complex landscape of student loans, optimize your repayment strategy, and ultimately save a substantial amount of money.

The year 2026 is a critical juncture for student loan borrowers, as new federal policies and adjustments are anticipated to come into full effect. These changes present both challenges and opportunities. Those who are proactive and informed will be best positioned to capitalize on these shifts, transforming potential liabilities into manageable and even accelerated pathways to financial freedom. Understanding the nuances of these changes, from interest rate caps to revised income-driven repayment (IDR) plans, is paramount.

Our goal is to demystify these complexities, providing a clear roadmap to reduce your student loan interest. We’ll delve into the foundational principles of student loan interest, explore the impact of recent and upcoming federal policies, and present a range of proven strategies—from refinancing to understanding specific loan programs—that can put more money back into your pocket. By the end of this article, you will have a robust understanding of how to approach your student loan debt with confidence and a clear plan for minimizing interest payments.

Understanding Student Loan Interest: The Basics

Before diving into advanced strategies, it’s crucial to grasp the fundamentals of how student loan interest works. Interest is essentially the cost of borrowing money, calculated as a percentage of the outstanding loan balance. This percentage can be fixed or variable, and its accumulation significantly impacts the total amount you repay.

Fixed vs. Variable Interest Rates

Most federal student loans come with fixed interest rates, meaning the rate remains the same throughout the life of the loan. This provides predictability in your monthly payments. Private student loans, however, can have either fixed or variable rates. Variable rates can fluctuate based on market conditions, potentially leading to higher payments if rates rise, but also offering lower initial rates.

Accrued Interest and Capitalization

Interest begins accruing on your loan from the moment it’s disbursed. For unsubsidized federal loans and all private loans, interest accrues while you’re in school, during grace periods, and during deferment or forbearance. If this accrued interest isn’t paid before the repayment period begins or ends, it can be capitalized. Capitalization means the unpaid interest is added to your principal balance, and future interest is then calculated on this larger amount—effectively leading to interest on interest. This is a major factor that increases the total cost of your student loan interest over time.

The Impact of Loan Servicers

Your loan servicer is the company that handles your student loan billing and other services. They play a crucial role in your repayment journey. While they don’t set interest rates, they implement the terms of your loan and can offer guidance on repayment plans, deferment, and forbearance options. Understanding how to effectively communicate with your servicer and knowing your rights as a borrower is vital for managing your student loan interest.

Navigating Federal Policy Changes for 2026

The landscape of federal student loan policy is dynamic, with significant reforms often taking several years to fully implement. As we approach 2026, several key changes are expected to solidify, offering both new challenges and unprecedented opportunities for borrowers to reduce their student loan interest.

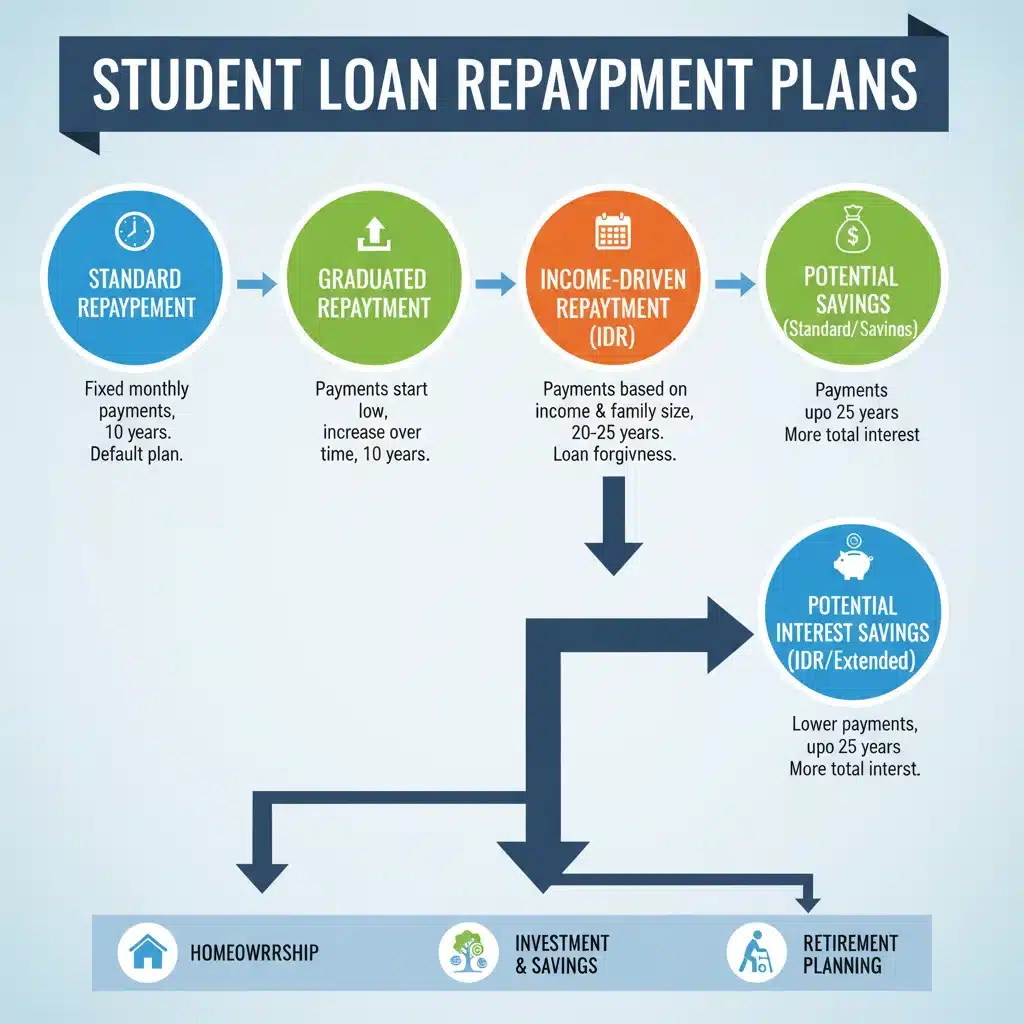

The SAVE Plan and Its Future Evolution

The Biden-Harris administration introduced the Saving on a Valuable Education (SAVE) Plan, an income-driven repayment (IDR) plan that offers significant benefits. While many aspects are already in effect, some of the most impactful provisions are scheduled for July 2024 and beyond, influencing how borrowers manage their student loan interest in the lead-up to 2026.

Key features of the SAVE Plan include:

- Reduced Monthly Payments: For undergraduate loans, monthly payments are calculated based on 5% of discretionary income, down from 10% on previous IDR plans. This significantly lowers the burden for many borrowers.

- Interest Subsidy: Perhaps the most revolutionary aspect for reducing student loan interest, the SAVE Plan prevents unpaid interest from accumulating. If your calculated monthly payment doesn’t cover the full amount of interest due, the government covers the remaining interest, preventing balance growth due to interest capitalization. This is a game-changer for many borrowers struggling with negative amortization.

- Shorter Path to Forgiveness: For borrowers with original principal balances of $12,000 or less, loan forgiveness can be achieved after just 10 years of payments, with an additional year added for every $1,000 borrowed above that threshold. This accelerated forgiveness can drastically reduce the total amount of student loan interest paid over time.

As 2026 approaches, it’s crucial to monitor any further refinements or expansions of the SAVE Plan. Staying enrolled or applying for the SAVE Plan if eligible is one of the most direct ways to benefit from federal relief and minimize your student loan interest.

Potential for Across-the-Board Interest Rate Adjustments

While less common, federal policy can sometimes introduce changes to how interest rates are set or capped for future loans, and in rare cases, even for existing loans. While a broad reduction for all existing loans is unlikely, specific programs or relief efforts might emerge that effectively lower the burden of student loan interest for certain groups of borrowers. Keep an eye on legislative proposals and announcements from the Department of Education.

Impact of Economic Factors on Federal Loan Rates

Federal student loan interest rates are set annually by Congress, typically tied to the 10-year Treasury note. While these are fixed for the life of the loan once disbursed, the economic climate leading up to 2026 could influence rates for new loans. Understanding these trends can help prospective students or those considering additional education make informed borrowing decisions to minimize future student loan interest.

Smart Strategies to Reduce Your Student Loan Interest by Up To 1.5%

Achieving a 1.5% reduction in your student loan interest can translate into thousands of dollars saved over the life of your loan. This section outlines actionable strategies, combining federal program utilization with smart personal finance moves.

1. Refinancing Private Student Loans

For borrowers with private student loans, refinancing is often the most direct and impactful way to reduce your student loan interest. Refinancing involves taking out a new loan, usually from a private lender, to pay off existing student loans. If you have improved your credit score, increased your income, or if market interest rates have dropped since you originally took out your loans, you could qualify for a significantly lower interest rate.

- Credit Score Improvement: Lenders view a higher credit score as less risky, leading to better interest rate offers.

- Income Growth: A stable and higher income demonstrates your ability to repay, making you a more attractive borrower.

- Market Rate Fluctuations: Keep an eye on general interest rate trends. If rates are low, it could be an opportune time to refinance.

Even a 0.5% to 1.0% reduction can lead to substantial savings. If you have excellent credit, you might even achieve the full 1.5% or more. However, be cautious: refinancing federal loans into private ones means losing access to federal benefits like IDR plans, deferment, forbearance, and potential forgiveness programs. This strategy is primarily recommended for private loans or for federal borrowers who are confident they won’t need federal protections.

2. Maximizing the SAVE Plan (Federal Loans)

As discussed, the SAVE Plan is a powerful tool for federal loan borrowers. Its interest subsidy feature directly combats the accumulation of unpaid student loan interest. If your income is relatively low compared to your loan balance, the SAVE Plan can effectively reduce your monthly payment and prevent your balance from growing due to interest. Ensure you are enrolled if eligible, and recertify your income annually to keep your payments accurate.

3. Making Extra Payments (Principal Reduction)

This is a straightforward yet highly effective strategy. Any extra money you pay towards your loan goes directly to reducing the principal balance. Since interest is calculated on the principal, a lower principal means less student loan interest accrues over time. Even small, consistent extra payments can make a big difference. Specify to your loan servicer that extra payments should be applied to the principal, not just advanced to the next month’s payment.

4. Bi-Weekly Payments

Instead of making one monthly payment, split your monthly payment in half and pay every two weeks. This results in 26 half-payments per year, which is equivalent to 13 full monthly payments instead of 12. That extra payment each year directly reduces your principal, leading to less student loan interest over the loan term.

5. Automating Payments for Interest Rate Reductions

Many loan servicers offer a small interest rate reduction (typically 0.25%) if you sign up for automatic debit payments. While this might seem minor, it’s a guaranteed reduction in your student loan interest that requires minimal effort. Over the life of a loan, this can add up to significant savings.

6. Public Service Loan Forgiveness (PSLF) and Other Forgiveness Programs

For those working in qualifying public service jobs, PSLF can lead to the forgiveness of your remaining federal Direct Loan balance after 120 qualifying monthly payments. While not a direct reduction in student loan interest, it eliminates the principal and any remaining interest, effectively saving you a massive amount. Other sector-specific forgiveness programs (e.g., for teachers, nurses, doctors) also exist and can offer substantial relief.

7. Employer Assistance Programs

A growing number of employers are offering student loan repayment assistance as a benefit. These programs can involve direct contributions to your loan principal or offer matching programs. Inquire with your HR department about any such benefits, as employer contributions effectively reduce your principal and, by extension, your student loan interest.

8. Utilizing Tax Deductions for Student Loan Interest

The IRS allows you to deduct the amount of student loan interest you paid during the year, up to a maximum of $2,500. This deduction can reduce your taxable income, indirectly saving you money that can then be applied back to your loans to further reduce your student loan interest. Keep accurate records of your interest payments for tax season.

Anticipating and Adapting to 2026 Federal Policy Landscape

The journey to reducing your student loan interest is ongoing, and staying informed about future policy shifts is crucial. The year 2026 isn’t just a finish line for current policies; it’s a potential starting point for new ones.

Monitoring Legislative Developments

Student loan policy is a frequent topic of discussion in Congress. Keep an eye on news from the Department of Education, legislative proposals, and advocacy groups. These sources can provide early warnings about potential changes that could impact your student loan interest or repayment strategy. Subscribing to official government newsletters or reputable financial news outlets can help you stay current.

Preparing for Potential Interest Rate Caps or Adjustments

While the SAVE Plan already offers an interest subsidy, there could be future discussions around broader interest rate caps for federal loans or new mechanisms to adjust rates in response to economic conditions. Understanding how these might affect your specific loan type is important. For instance, if you have older federal loans with higher fixed rates, any future policy offering a reduction could be highly beneficial.

The Evolving Role of Income-Driven Repayment Plans

IDR plans have evolved significantly over the past decade, and this trend is likely to continue. The SAVE Plan is the current benchmark, but future administrations or legislative bodies might introduce new IDR options or modify existing ones. Understanding the details of each plan and how they calculate discretionary income and monthly payments is key to minimizing your student loan interest and achieving forgiveness.

Leveraging Financial Literacy and Counseling

As policies become more complex, the value of financial literacy and professional counseling increases. Non-profit credit counseling agencies and certified financial planners specializing in student loan debt can provide personalized advice. They can help you understand your options, compare repayment plans, and develop a tailored strategy to reduce your student loan interest in the context of your unique financial situation and the evolving federal landscape.

Case Studies: Realizing Interest Savings

To illustrate the power of these strategies, let’s consider a few hypothetical scenarios where borrowers successfully reduced their student loan interest.

Case Study 1: The Refinancing Success Story

Sarah graduated with $60,000 in private student loans at an average interest rate of 7.5%. After three years of working, she had built an excellent credit score of 780 and secured a stable job. She decided to refinance her loans. She qualified for a new loan with a fixed interest rate of 5.0%. This 2.5% reduction (well over our target 1.5%) saved her approximately $8,000 over a 10-year repayment term, and significantly reduced her monthly payment. Her total student loan interest paid was dramatically lowered.

Case Study 2: The SAVE Plan Champion

David, a recent graduate with $35,000 in federal student loans, started a job with a modest income. His standard repayment plan payment was unaffordable, and he saw his loan balance growing due to accruing interest. He enrolled in the SAVE Plan. His calculated monthly payment was low enough that the government began covering all of his unpaid interest each month. This prevented his balance from growing and effectively capped his student loan interest burden, allowing him to focus on gradually reducing his principal.

Case Study 3: The Strategic Extra Payer

Maria had $45,000 in federal student loans at 6.0% interest. She couldn’t refinance her federal loans without losing benefits, but she had a bit of extra income each month. Instead of just making her minimum payments, she committed to paying an extra $50 per month directly to her principal. Over the 10-year term, this seemingly small extra payment resulted in her paying off her loan nearly a year earlier and saving over $1,500 in total student loan interest.

Common Pitfalls to Avoid When Reducing Student Loan Interest

While many strategies can help reduce your student loan interest, it’s equally important to be aware of common mistakes that can derail your efforts or even worsen your financial situation.

1. Refinancing Federal Loans Without Understanding the Trade-offs

As mentioned, refinancing federal loans into private loans means forfeiting critical federal protections like income-driven repayment plans, extensive deferment/forbearance options, and eligibility for federal loan forgiveness programs (like PSLF). If you anticipate needing these safety nets, or if there’s a chance you might qualify for forgiveness, think twice before refinancing federal loans, even for a lower interest rate. The potential loss of flexibility might outweigh the student loan interest savings.

2. Ignoring Accruing Interest During Deferment or Forbearance

While deferment and forbearance can provide temporary relief from payments, interest often continues to accrue, especially on unsubsidized federal loans and all private loans. If this interest is not paid, it can be capitalized (added to your principal) once your deferment/forbearance period ends. This significantly increases your total student loan interest burden. If you must use these options, try to make interest-only payments if possible to prevent capitalization.

3. Not Recertifying Income Annually for IDR Plans

If you are on an Income-Driven Repayment (IDR) plan like SAVE, PAYE, or IBR, you must recertify your income and family size annually. Failing to do so can result in your payments reverting to the higher standard repayment amount, and any unpaid interest that was previously subsidized could be capitalized, increasing your principal and future student loan interest.

4. Falling for Scams

Be wary of companies promising instant loan forgiveness or guaranteed interest rate reductions for a fee. Legitimate student loan assistance is available directly through your loan servicer or the Department of Education, usually for free. Never pay an upfront fee for services you can get for free or for promises that seem too good to be true. These scams often target borrowers struggling with high student loan interest.

5. Not Shopping Around for Refinancing

If you decide to refinance private loans, don’t just accept the first offer you receive. Apply with multiple lenders to compare interest rates, terms, and any associated fees. A few percentage points difference in your new student loan interest rate can save you thousands over the life of the loan. Use pre-qualification tools that don’t impact your credit score to get a sense of your options.

6. Avoiding Communication with Your Loan Servicer

Your loan servicer is there to help you understand your options. If you’re struggling to make payments, facing financial hardship, or simply want to explore different repayment plans to reduce your student loan interest, contact them. They can guide you through available federal programs and options like deferment, forbearance, or IDR plans before you fall behind on payments.

7. Neglecting Your Credit Score

Your credit score is a major factor in determining the interest rates you qualify for when refinancing private loans. Poor credit can either prevent you from refinancing or result in a higher interest rate than you currently have. Focus on building and maintaining a good credit score (paying bills on time, keeping credit utilization low) to ensure you can access the best possible rates for reducing your student loan interest.

8. Underestimating the Power of Small, Consistent Payments

It’s easy to dismiss small extra payments as insignificant. However, as demonstrated in our case studies, consistently paying even a little extra each month can significantly reduce the principal balance over time, leading to substantial savings on total student loan interest. Don’t let the idea that you need to make huge extra payments deter you from making any at all.

Preparing for the Future: Long-Term Financial Health Beyond 2026

Reducing your student loan interest by up to 1.5% by 2026 is an excellent short-to-medium term goal, but true financial freedom requires a long-term perspective. As you implement these strategies, consider how they fit into your broader financial health.

Building an Emergency Fund

Having an emergency fund (3-6 months of living expenses) is crucial. It acts as a buffer against unexpected financial setbacks, reducing the likelihood that you’ll need to pause student loan payments (which can lead to interest capitalization) or take on new high-interest debt.

Investing for the Future

Once you’ve optimized your student loan payments and reduced your student loan interest, redirecting those savings towards investments (e.g., retirement accounts, brokerage accounts) can accelerate your wealth building. The power of compound interest works in your favor when investing, just as it works against you with debt.

Continuous Education on Financial Topics

The financial landscape, especially concerning student loans, is constantly evolving. Commit to continuous learning about personal finance, investment strategies, and changes in federal policy. This ongoing education will empower you to make informed decisions and adapt your strategies as needed.

Understanding Your Overall Debt Picture

Student loans are often just one piece of the puzzle. Consider your entire debt portfolio—credit cards, auto loans, mortgages—and how they interact. Prioritizing high-interest debt (like credit cards) while strategically managing your student loan interest can create a more holistic approach to debt reduction.

By integrating these strategies into a comprehensive financial plan, you’re not just saving on student loan interest; you’re building a foundation for lasting financial security and achieving your long-term goals.

Conclusion: Taking Control of Your Student Loan Interest

The prospect of reducing your student loan interest by up to 1.5% in 2026, amidst evolving federal policies, is not merely a hopeful aspiration but an achievable goal for informed and proactive borrowers. By understanding the mechanics of interest, staying abreast of federal programs like the SAVE Plan, and implementing smart financial strategies, you can significantly lighten your debt burden.

From strategically refinancing private loans to making extra payments, utilizing employer benefits, and leveraging tax deductions, each step you take contributes to a healthier financial future. Remember the importance of continuous vigilance: federal policies can shift, and market conditions change, necessitating ongoing attention to your repayment strategy.

Don’t let the complexity of student loan debt paralyze you. Take control by educating yourself, utilizing available resources, and making deliberate decisions. The savings you achieve on student loan interest can free up financial resources for other life goals, bringing you closer to true financial independence. Start planning today, and set yourself up for success in 2026 and beyond.