Federal Housing Market Forecast 2026: Opportunities & Risks for Homebuyers

The landscape of homeownership is perpetually shifting, influenced by a complex interplay of economic indicators, demographic changes, and governmental policies. As we look ahead to the housing market 2026, prospective homebuyers, current homeowners, and real estate investors are all seeking clarity amidst the uncertainties. This comprehensive analysis aims to dissect the federal housing market forecast for 2026, pinpointing the opportunities that may arise and the risks that demand careful consideration. Understanding these dynamics is crucial for making informed decisions in an evolving real estate environment.

The past few years have been a rollercoaster for the housing sector. From the pandemic-induced boom fueled by historically low interest rates and a sudden demand for more space, to the subsequent cooldown driven by aggressive rate hikes, the market has demonstrated remarkable volatility. As we approach 2026, the federal housing market is expected to settle into a new equilibrium, but not without its challenges and rewards. This article will delve into the macroeconomic factors, supply and demand dynamics, regulatory influences, and emerging trends that will shape the housing market 2026.

Understanding the Macroeconomic Underpinnings of the Housing Market 2026

The federal housing market does not exist in a vacuum; it is intricately linked to broader macroeconomic conditions. Several key indicators will play a pivotal role in defining the trajectory of the housing market 2026. These include inflation, interest rates, employment figures, and overall economic growth.

Inflation and its Impact

Inflation has been a dominant theme in recent economic discussions. While central banks have been working diligently to bring inflation down to target levels, its lingering effects can still influence housing affordability. High inflation erodes purchasing power, making it more challenging for potential homebuyers to save for down payments and manage monthly mortgage payments. However, if inflation stabilizes and returns to more historical norms by 2026, it could provide a more predictable economic environment, fostering greater confidence among buyers and sellers.

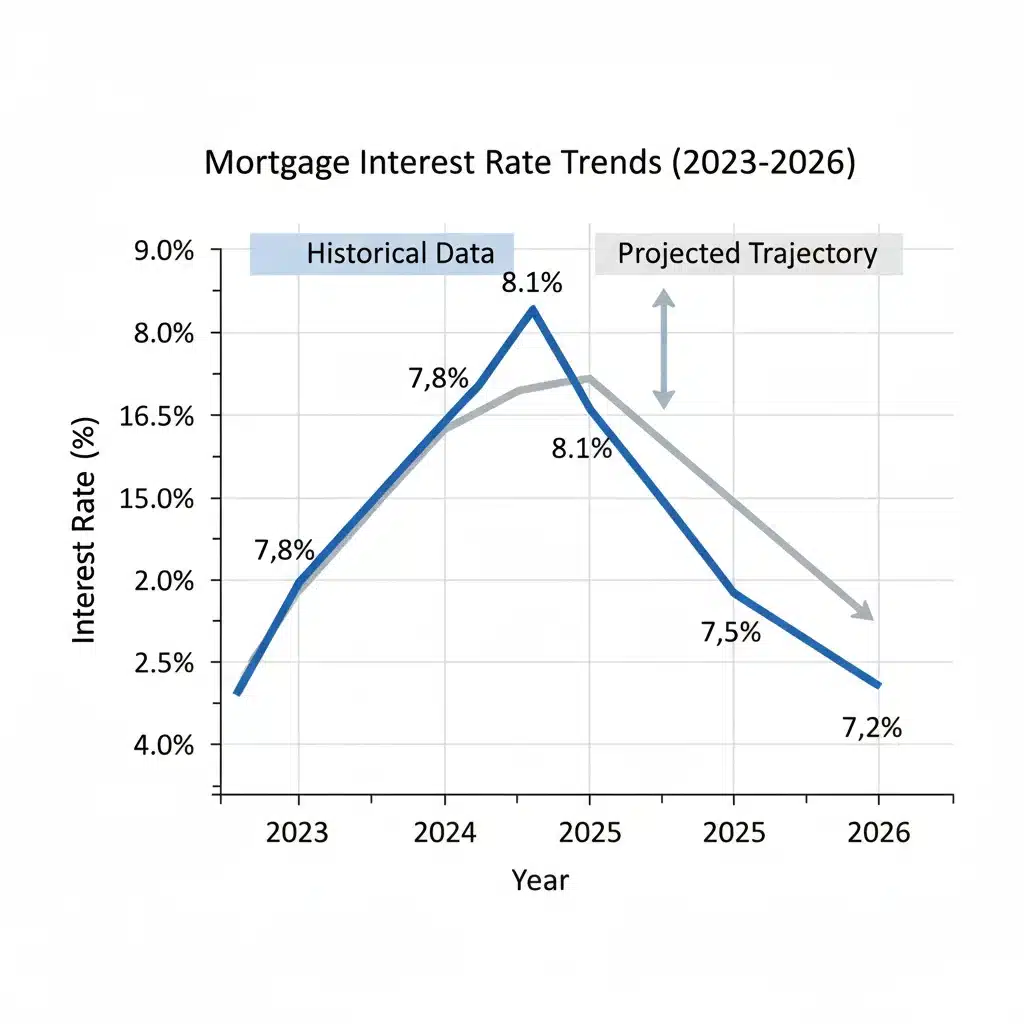

Interest Rate Projections

Perhaps no single factor impacts the housing market as directly as interest rates. The rapid increase in mortgage rates over the past couple of years has significantly cooled demand and reduced affordability. Looking towards 2026, the consensus among many economists is that interest rates may stabilize or even see a slight decline, assuming inflation remains under control. A more predictable and potentially lower interest rate environment would undoubtedly be a boon for the housing market 2026, making homeownership more accessible and stimulating buyer activity. However, any unexpected resurgence in inflation could prompt central banks to maintain higher rates, presenting a substantial risk.

Employment and Wage Growth

A robust job market with consistent wage growth is fundamental to a healthy housing market. When people are employed and earning more, they have the financial capacity and confidence to invest in real estate. The federal housing market in 2026 will heavily rely on the continued strength of the labor market. While some sectors may experience shifts, overall employment stability and moderate wage increases are anticipated to support housing demand. Conversely, a significant economic downturn or widespread job losses could suppress demand and lead to a softer market.

Gross Domestic Product (GDP)

Overall economic growth, measured by GDP, provides a broad indicator of economic health. A growing economy generally translates to a more dynamic housing market. As the economy expands, consumer confidence tends to rise, and investment opportunities become more attractive. For the housing market 2026, a steady, albeit potentially moderate, GDP growth rate would provide a stable foundation, encouraging both new construction and transactions in the existing home market.

Supply and Demand Dynamics in the Housing Market 2026

The fundamental principles of supply and demand remain central to understanding price movements and market activity. The federal housing market in 2026 will be shaped by ongoing trends in housing inventory and buyer demand.

Housing Inventory: A Persistent Challenge

For several years, the housing market has struggled with a chronic shortage of available homes, particularly in desirable urban and suburban areas. This low inventory has been a primary driver of price appreciation. While new construction has picked up in some regions, it has yet to fully alleviate the supply crunch. Factors contributing to this include:

- Builder Challenges: High material costs, labor shortages, and regulatory hurdles continue to impact the pace of new home construction.

- Existing Homeowner Reluctance: Many homeowners who locked in historically low mortgage rates are reluctant to sell, as doing so would mean taking on a new mortgage at a higher rate. This ‘golden handcuff’ effect contributes to fewer existing homes coming onto the market.

- Aging Housing Stock: A significant portion of the housing stock in the U.S. is aging, requiring substantial investment for modernization, which can deter some sellers or buyers.

By 2026, it is anticipated that inventory levels may improve marginally, but a significant oversupply is unlikely. This continued tightness in supply will likely keep upward pressure on home prices, albeit at a more sustainable pace than seen during the pandemic boom. For the housing market 2026, this means that while bidding wars might become less common, well-located and well-maintained properties will still command strong interest.

Buyer Demand: Demographic Shifts and Affordability

Despite affordability challenges, underlying demand for housing remains robust. Several demographic trends are contributing to this sustained interest:

- Millennials and Gen Z: These large generations are increasingly entering their prime home-buying years. As they form families and seek stable living situations, their demand for housing will continue to be a significant market driver.

- Migration Patterns: Shifting work models and preferences for certain lifestyles are leading to continued migration patterns, with some regions experiencing heightened demand.

- Household Formation: The rate of new household formation remains strong, translating directly into a need for more housing units.

However, affordability remains a critical hurdle. High home prices coupled with elevated interest rates have priced many potential buyers out of the market. The housing market 2026 will likely see a continued emphasis on creative financing options, down payment assistance programs, and a greater focus on more affordable housing types, such as townhouses and condominiums, particularly in competitive markets.

Opportunities for Homebuyers in the Housing Market 2026

While the market may present challenges, 2026 is also expected to offer distinct opportunities for savvy homebuyers. Understanding these can help individuals strategically navigate their path to homeownership.

Stabilizing Interest Rates

As mentioned, the potential for stabilizing or slightly declining interest rates presents a significant opportunity. Even a modest reduction in mortgage rates can lead to substantial savings over the life of a loan and improve monthly affordability. Homebuyers should closely monitor Federal Reserve policies and economic indicators to anticipate these shifts. Locking in a favorable rate in 2026 could provide long-term financial benefits.

Less Frenzied Competition

The intense bidding wars and waived contingencies that characterized the pandemic-era market are largely a thing of the past. The housing market 2026 is expected to be more balanced, offering buyers more time to make decisions, conduct thorough inspections, and negotiate terms. This creates a less stressful buying experience and allows for more prudent financial planning.

Increased Inventory in Specific Segments

While overall inventory may remain tight, certain segments of the market could see improved supply. This might include:

- New Construction: As builders adapt to market conditions and supply chain issues ease, more new homes, particularly in master-planned communities, could become available. These often come with modern amenities and energy efficiencies.

- Condominiums and Townhouses: These housing types often offer a more affordable entry point into homeownership, especially in urban and densely populated suburban areas. Increased development in these segments could provide more options.

- Secondary Markets: Some secondary and tertiary markets, which saw rapid growth during the pandemic, might experience a slight cooling, leading to more balanced inventory levels and potentially more competitive pricing.

Focus on Long-Term Value

The housing market 2026 will likely reward buyers who focus on long-term value rather than short-term gains. Properties in areas with strong economic fundamentals, good schools, and developing infrastructure are likely to appreciate steadily. Buyers who prioritize these aspects will be better positioned for sustained equity growth.

Risks and Challenges in the Housing Market 2026

Despite the opportunities, several risks and challenges will persist in the housing market 2026. Homebuyers must be aware of these to mitigate potential negative impacts.

Lingering Affordability Issues

Even with potential rate stabilization, home prices remain historically high in many regions. This, combined with any continued elevated interest rates, means affordability will remain a significant challenge for many. The income-to-home price ratio is still stretched, particularly for first-time buyers. This could lead to:

- Delayed Homeownership: Many individuals and families may need to save longer for a down payment.

- Relocation: Buyers might be forced to consider less expensive geographic areas or smaller homes than initially desired.

- Reliance on Assistance Programs: Increased reliance on federal and state first-time homebuyer programs will be crucial for many.

Economic Volatility and Recession Fears

While a soft landing is the hoped-for scenario, the risk of an economic downturn or recession cannot be entirely discounted. A significant economic contraction could lead to job losses, reduced consumer confidence, and a tightening of lending standards. Such conditions would undoubtedly dampen demand in the housing market 2026 and could put downward pressure on home values in some areas.

Geopolitical Events and Global Economic Shocks

The interconnectedness of the global economy means that geopolitical events, such as conflicts or supply chain disruptions, can have ripple effects on the U.S. housing market. These events can impact inflation, interest rates, and overall economic stability, introducing an element of unpredictability. While difficult to forecast, staying informed about global developments is prudent for anyone looking to enter the housing market 2026.

Climate Change and Insurance Costs

An increasingly prominent risk factor, particularly in certain regions, is the growing impact of climate change. Increased frequency and intensity of natural disasters (e.g., wildfires, floods, hurricanes) are leading to escalating home insurance costs, and in some extreme cases, a withdrawal of insurers from high-risk areas. This can significantly impact the long-term cost of homeownership and the desirability of certain properties, a factor that will become even more critical in the housing market 2026 and beyond.

Regional Variations in the Housing Market 2026

It is crucial to remember that the federal housing market is not monolithic. Conditions can vary dramatically from one region to another, and even within different neighborhoods of the same city. What might be an opportunity in one area could be a significant risk in another.

Growth Markets vs. Stagnant Markets

Some regions, particularly those with strong job growth in tech, healthcare, or green energy sectors, are likely to continue experiencing robust demand and price appreciation. Conversely, areas with declining populations or struggling economies might see more stagnant or even depreciating home values. Homebuyers in the housing market 2026 should conduct thorough local market research.

Urban vs. Suburban vs. Rural

The pandemic initially spurred a migration to suburban and rural areas as remote work became prevalent. While some of this trend has reversed, a hybrid work model means that demand for homes outside traditional urban cores remains strong. While urban centers are also seeing a resurgence, the housing market 2026 will likely see continued competition across all segments, with specific preferences varying by individual and family needs.

Navigating the Housing Market 2026: Strategies for Homebuyers

Given the opportunities and risks, what strategies can homebuyers employ to succeed in the housing market 2026?

Financial Preparedness is Key

This cannot be overstated. Saving a substantial down payment, improving your credit score, and getting pre-approved for a mortgage are foundational steps. Understanding your budget thoroughly and accounting for all associated costs (closing costs, property taxes, insurance, maintenance) will prevent unexpected financial strain.

Patience and Flexibility

The days of rapid home appreciation might be tempered in 2026. Buyers who are patient and flexible with their criteria (e.g., considering different neighborhoods, smaller homes, or fixer-uppers) may find better deals. Avoid making rushed decisions driven by fear of missing out.

Leverage Technology and Local Expertise

Utilize online tools and resources to research market trends, property values, and neighborhood statistics. However, complement this with the invaluable insights of experienced local real estate agents who have a pulse on specific market conditions and can identify emerging opportunities or risks.

Consider All Financing Options

Explore various mortgage products, including adjustable-rate mortgages (ARMs) if appropriate for your financial situation, or government-backed loans like FHA or VA loans, which often have more lenient down payment requirements. Research local and federal first-time homebuyer assistance programs.

Don’t Overlook New Construction

If existing home inventory remains tight, new construction could be a viable option. Builders may offer incentives, and new homes often come with warranties and modern features that can save on maintenance costs in the short term. Additionally, new developments can sometimes be found in areas poised for future growth.

Focus on Long-Term Investment Potential

While short-term market fluctuations are inevitable, homeownership is typically a long-term investment. Focus on properties that meet your needs for the foreseeable future and are located in areas with strong fundamentals that support long-term appreciation. Don’t chase trends; invest in quality and location.

The Role of Government and Policy in the Housing Market 2026

Federal and local government policies will continue to play a significant role in shaping the housing market 2026. Initiatives aimed at increasing housing supply, promoting affordability, and addressing homelessness will have direct impacts.

Affordable Housing Initiatives

Expect continued efforts from federal, state, and local governments to address the affordable housing crisis. This could include grants for developers building affordable units, tax incentives, zoning reforms to allow for higher density, and expanded rental assistance programs. Such initiatives, while primarily targeting lower-income segments, can indirectly alleviate pressure on the broader market by increasing overall housing availability.

Zoning and Land Use Reforms

Many areas face restrictive zoning laws that limit housing density and drive up development costs. There is a growing push at various governmental levels to reform these regulations to allow for more diverse housing types, such as duplexes, townhouses, and accessory dwelling units (ADUs). Successful implementation of these reforms could significantly boost housing supply in the long run, impacting the housing market 2026 and beyond.

Infrastructure Investment

Federal infrastructure spending can have a profound impact on real estate development. Investments in transportation, utilities, and public amenities can make previously less desirable areas more attractive for both residents and developers, potentially opening up new housing markets and reducing pressure on existing ones. Areas benefiting from such investments could present emerging opportunities for homebuyers.

Conclusion: A Balanced Outlook for the Housing Market 2026

The federal housing market forecast for 2026 suggests a period of normalization and stabilization, albeit with persistent challenges. While the extreme volatility of recent years may subside, affordability will remain a key concern, driven by high prices and the ongoing battle against inflation. However, potential stabilization or even slight easing of interest rates, coupled with less frenzied competition, will present opportunities for well-prepared buyers.

For those looking to enter the housing market 2026, success will hinge on diligent financial planning, thorough research into local market conditions, and a willingness to be patient and adaptable. Understanding the broader macroeconomic trends, the dynamics of supply and demand, and the influence of governmental policies will be crucial. By carefully weighing the opportunities against the risks, homebuyers can navigate the evolving real estate landscape effectively and make sound, long-term investments in their future.

Ultimately, 2026 is unlikely to be a return to the pre-pandemic market, nor will it replicate the frenzied highs. Instead, it is poised to be a more mature and perhaps more predictable market, demanding strategic thinking and informed decision-making from all participants. The key takeaway is to approach the housing market 2026 with a clear understanding of your financial capabilities, a realistic perspective on market conditions, and a readiness to seize opportunities as they arise.